Crypto expert Benjamin Cowen believes Bitcoin just dodged a big drop. In his latest analysis, he explains that Bitcoin closed the weekly candle just above the key “bull market support band,” even though it briefly fell below it. This support band is an important level that shows whether Bitcoin is in a bull or bear market.

Benjamin Cowen says as long as Bitcoin stays above this support band, it will likely avoid a major drop. The band is made up of the 20-week simple moving average (SMA) and the 21-week exponential moving average, which reflect the overall market mood.

Bitcoin Holds Key Support, But Challenges Remain: Analyst Urges Caution

In past bull markets, Bitcoin has often bounced back from this support band, signaling that a correction is over and more gains are likely. However, it’s important to stay cautious despite Benjamin Cowen’s optimistic view.

Bitcoin has shown volatility in this area before, and quick dips below the support band can cause brief panic among traders.

While holding the band is a good sign for Bitcoin, it doesn’t guarantee a fast recovery. With ongoing economic uncertainty and low trading volume, Bitcoin could face resistance in the coming weeks. It still hasn’t broken through key levels like $65,000. Also, if the Federal Reserve tightens its monetary policy, it could affect risk assets, including cryptocurrencies.

In short, Cowen’s outlook is positive, but we should be careful. For a stronger rally, Bitcoin needs to stay above the support band while managing outside challenges.

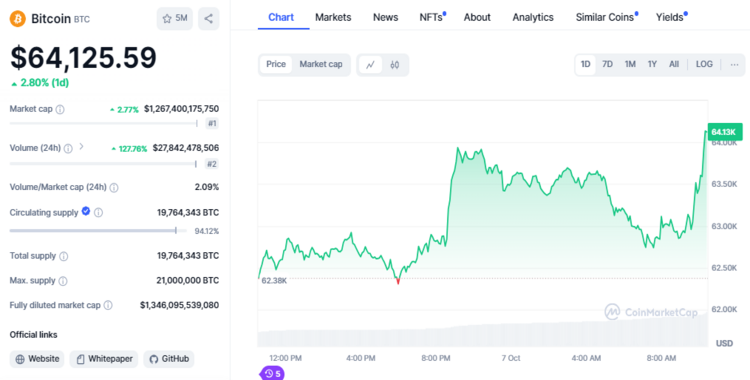

At the time of writing Bitcoin BTC is trading around $64100 and its up over 2.5% in last 24 hours as per Coinmarketcap data. Bitcoin is trading over $27 billion and its up over 120% as compare to last 24 hours.

Moreover, Ethereum and Solana are also up about 1.5%, 2.3% respectively.

#Bitcoin News #Bitcoin Price #Bitcoin Price Analysis #Bitcoin Price Prediction